loading...

AI Creator Economy (Part 1): Mapping the New Digital Ecosystem

Dinis GuardaAuthor

Fri Feb 27 2026

Explore the Creator Economy 360 framework by Dinis Guarda, mapping the $250B creator ecosystem, its three core pillars, segmentation models, AI impact, and the 90/10 rule shaping digital success.

The Creator Economy 360: Mapping the New Digital Ecosystem

The creator economy has quietly become one of the most significant economic shifts of the past two decades. What began as a handful of YouTubers and bloggers monetising their hobbies has evolved into a global ecosystem of over 404 million potential creators, spanning artists, software developers, educators, athletes, coaches, and entrepreneurs, all building businesses around content, community, and technology.

This is not a niche phenomenon. With a current market value estimated at $250 billion and projected to reach $500 billion by 2027, the creator economy is operating at a scale that rivals entire traditional industries. And yet, despite its size, most people inside it and many observing it from the outside , lack a clear framework for understanding how it actually works.

The Creator Economy 360 Elements Framework, developed by Dinis Guarda in 2025, addresses that gap. It maps the full complexity of the ecosystem, its players, its structures, its economic flows, and its contradictions, into a coherent model that creators, platforms, and businesses can use to orient themselves and build strategically.

Today we will cover the landscape: the three pillars that hold the ecosystem together, the different types of creators operating within it, and the hard statistical realities that define who succeeds and who doesn't.

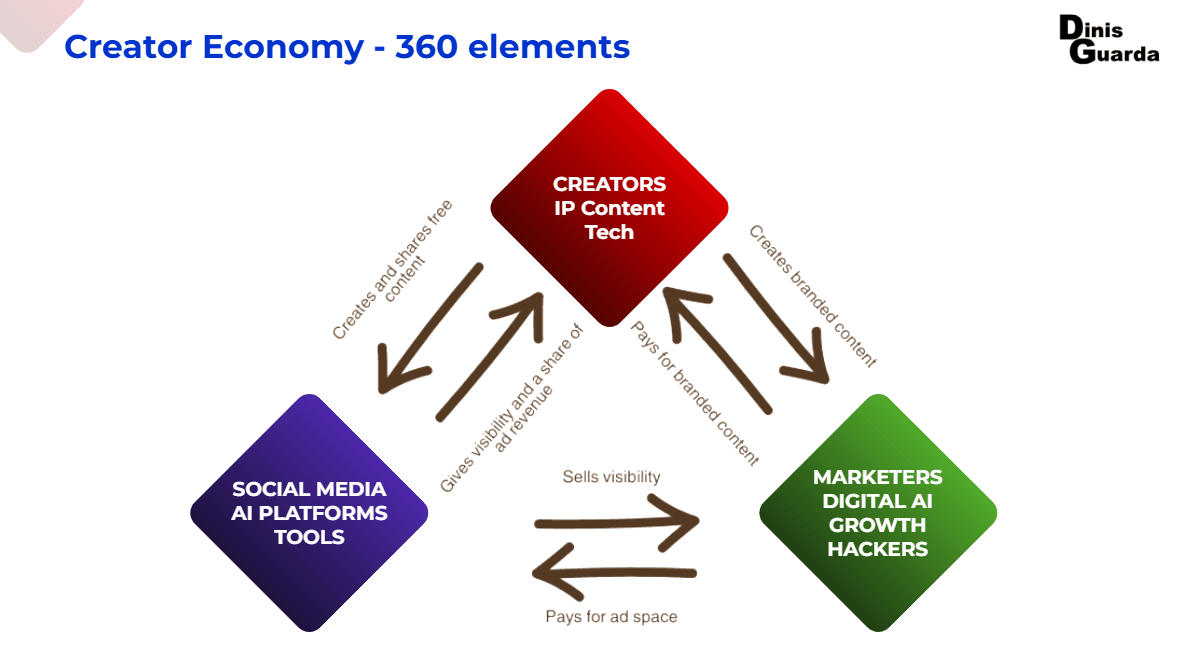

The Three Pillars: How the Creator Economy Actually Works

At the foundation of the 360 Elements Framework are three interconnected pillars. Understanding how they relate to each other is essential to understanding why the creator economy works the way it does.

- Creators IP, Content and Technology

Creators are the engine. They produce content, build audiences, and generate the intellectual property that gives the entire ecosystem its value. A creator's core asset is not their follower count, it is their IP: their voice, their perspective, their relationship with their audience, and increasingly, their ability to leverage technology to produce and distribute content at scale. AI tools are rapidly becoming central to this, enabling creators to produce more, faster, without requiring deep technical expertise.

- Social Media AI Platforms and Tools

Platforms are the infrastructure that connects creators to audiences and advertisers. They provide visibility, distribution, and in exchange, a share of the advertising revenue that creators help generate. Platforms have evolved dramatically from simple publishing tools into sophisticated AI-powered systems that shape what content gets seen, by whom, and when. This gives platforms enormous power over creator success, which is precisely why the movement toward creator-owned audiences and direct monetisation has become so important.

- Marketers Digital AI Growth Hackers

Marketers complete the economic triangle. They pay platforms for advertising space and pay creators for branded content. As AI reshapes marketing workflows, this group is growing rapidly ,with estimates suggesting 10 to 15 million people globally work in broadly defined marketing roles, and 83.2% of them planning to use AI tools for content creation. Marketers are not passive buyers in this system. They are active participants shaping what content gets made, how it is distributed, and what economic value flows back to creators.

The relationship between these three pillars creates the central economic loop of the creator economy: creators produce content that attracts audiences; platforms monetise those audiences through advertising; marketers pay for that access and commission creators directly. It is a self-reinforcing system , but one where the distribution of value is far from equal.

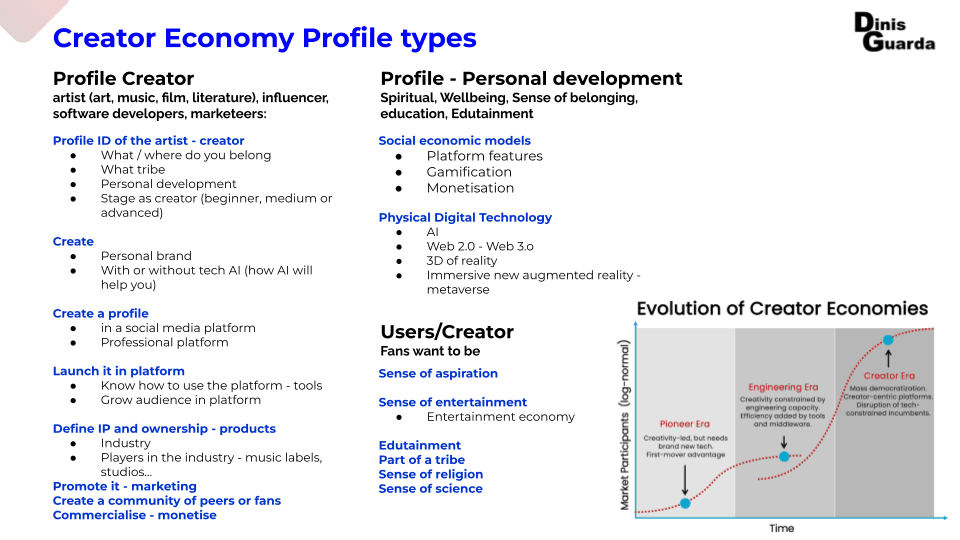

Creator Segmentation, Not All Creators Are the Same

One of the most useful aspects of the 360 Elements Framework is its refusal to treat "creators" as a single category. The reality is a diverse and stratified landscape, mapped across two dimensions: popularity and depth of specialisation.

- Power Super Ecosystem Creators operate at the top of the matrix, broad reach, multi-platform presence, high popularity, and the ability to command significant brand partnership revenues. These are the creators who have built genuine media businesses around their personal brand.

- Niche Expert Segments Creators trade breadth for depth. They have highly engaged audiences within specific domains, personal finance, health and wellness, software development, sustainable living, and their authority within their niche often makes them more commercially valuable per follower than mass-market creators. Brands increasingly prefer them for their precision targeting and audience trust.

- One Segment Expertise Reels Creators have mastered a single format in a specific topic area , typically short-form video. Their strength is consistency, platform optimisation, and the ability to generate high engagement within a defined content lane. They are specialists in the attention economy.

- Emergent New Creators are at the beginning of their journey. They represent the largest pool of future ecosystem participants and, critically, the segment that new platforms and tools are most designed to serve. Many will not progress beyond this stage, but those who do represent the next generation of the creator economy's power players.

Creator Profile Types, The Full Spectrum

Beyond the segmentation matrix, the framework maps creators by the type of work they do and the industry they operate in. This matters because each profile type has fundamentally different needs, monetisation paths, and platform strategies.

- Artists — musicians, filmmakers, visual artists, authors, and legacy artists — are perhaps the original creators, now navigating the intersection of traditional IP structures and new digital distribution models. A musician today must understand streaming royalties, social media algorithms, NFT potential, and direct fan monetisation simultaneously.

- Software Developers are an increasingly important and underrecognised creator category. They build the tools, games, and platforms that others use — and the creator economy is beginning to develop models that reward this kind of technical creation more directly, particularly through open APIs, blockchain reward systems, and developer-focused community platforms.

- Influencers, Celebrities, and Commentators operate across B2B and B2C models, often simultaneously. A business commentator on LinkedIn is as much a creator as a lifestyle influencer on Instagram — the platforms differ, but the underlying economics of audience, trust, and monetisation are the same.

- Designers and Technical Producers sit at the intersection of creativity and technical execution. As AI tools democratise basic design, this group is evolving, the value shifts from production to creative direction, brand strategy, and the ability to use AI tools to produce at a scale previously impossible for individuals.

- Wellbeing Personalities and Coaches represent one of the fastest-growing segments of the creator economy, driven by global demand for mental health content, fitness, nutrition, and personal development. Their monetisation models ,courses, memberships, events, 1:1 coaching tend to be more direct and less dependent on advertising than entertainment-focused creators.

- Agencies, Publishers, and Copyright Organisations are the B2B layer of the creator ecosystem. They manage talent, protect IP, distribute content, and increasingly function as technology businesses themselves, integrating AI tools, data analytics, and platform partnerships into their operations.

Each of these profile types requires a different strategic approach. The framework's value is in acknowledging this diversity rather than collapsing it into a single "creator" archetype.

The 90/10 Rule, The Hard Truth About Who Actually Creates

Perhaps the most important, and uncomfortable, insight in the 360 Elements Framework is what I call the 90/10 Rule. It describes the actual distribution of participation across the internet:

90% of internet users are passive consumers. They watch, scroll, read, and absorb, but they never create. 10% engage actively, commenting, sharing, curating, participating in communities. 1% are genuine content creators, producing original material with intention and consistency. And just 0.1% reach super creator status, the small group with significant audiences, meaningful influence, and real revenue generation.

This is not a temporary imbalance that will correct itself as platforms improve. It is a structural feature of digital participation. And it has profound implications for anyone trying to understand the creator economy honestly.

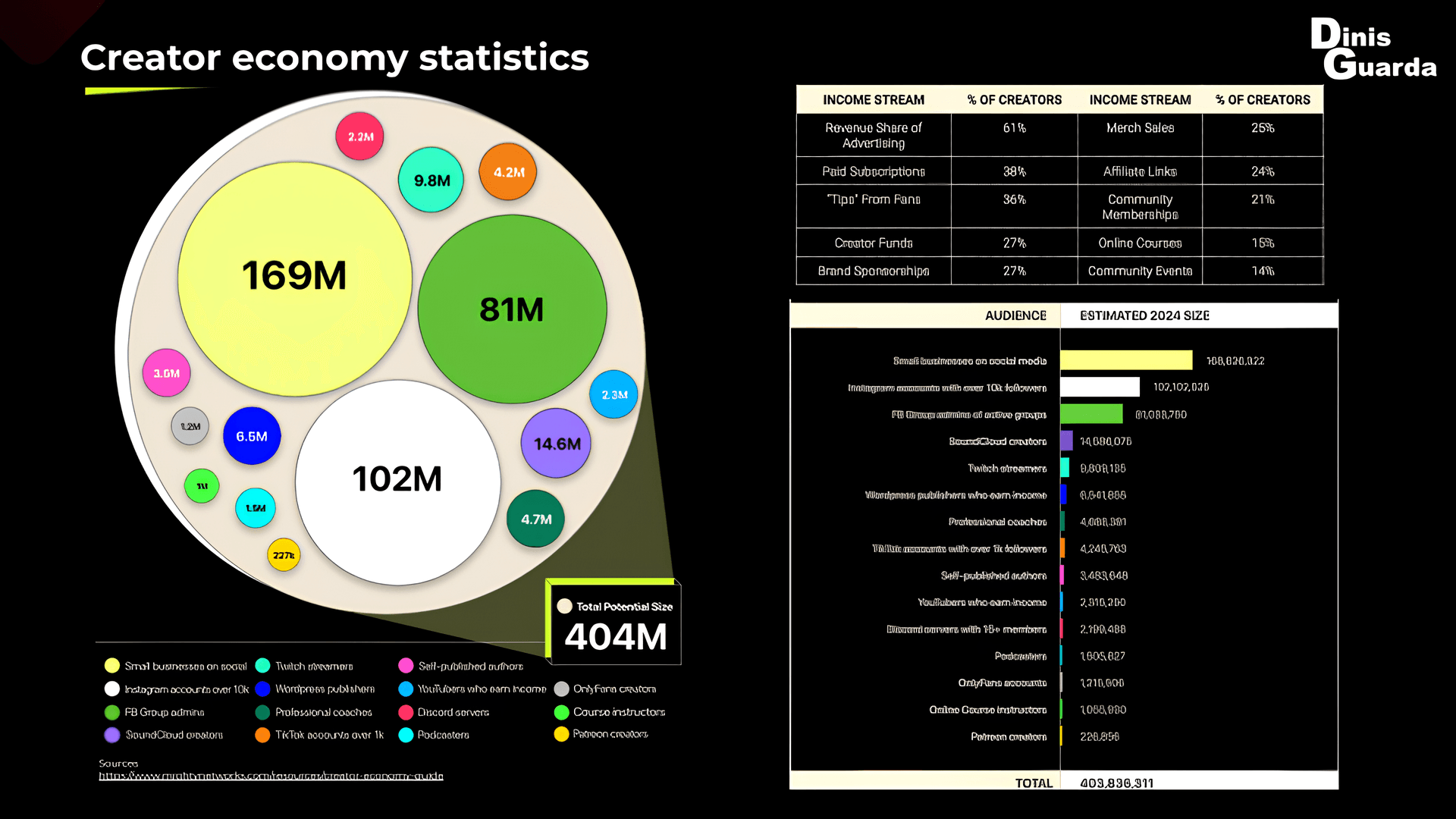

The 404 million figure that defines the total potential creator ecosystem includes 169 million small businesses on social media, 102 million Instagram accounts with over 10,000 followers, 81 million Facebook Group admins, 9.8 million Twitch streamers, and 227,000 Patreon creators. These are very different types and levels of "creator" and the revenue reality reflects that. 61% of creators rely on advertising revenue sharing as their primary income. Only 25% achieve meaningful merchandise sales. Only 15% generate income through online courses.

The creator economy's greatest promise, that anyone can build a sustainable livelihood from their creativity, remains real. But the 90/10 rule is a necessary corrective to the more utopian narratives. The path from consumer to creator to sustainable creative business is real, but it is not automatic, and it is not equal.

The Numbers, A Statistical Portrait of the Ecosystem

The following data points frame the current state of the creator economy and the broader gig economy it is converging with.

The global creator community exceeds 207 million individuals, approximately 162 million amateurs and 45 million professionals. The largest single segment is the nano-influencer category: 139 million creators with between 1,000 and 10,000 followers, semi-professional participants sitting at the intersection of authenticity and emerging commercial viability.

AI adoption within the creator community is already mainstream. 83% of Instagram influencers have used AI tools for content creation, primarily for images, videos, and captions. Over 60% of all creators regularly integrate AI into their workflows. This is not a future trend, it is the current baseline.

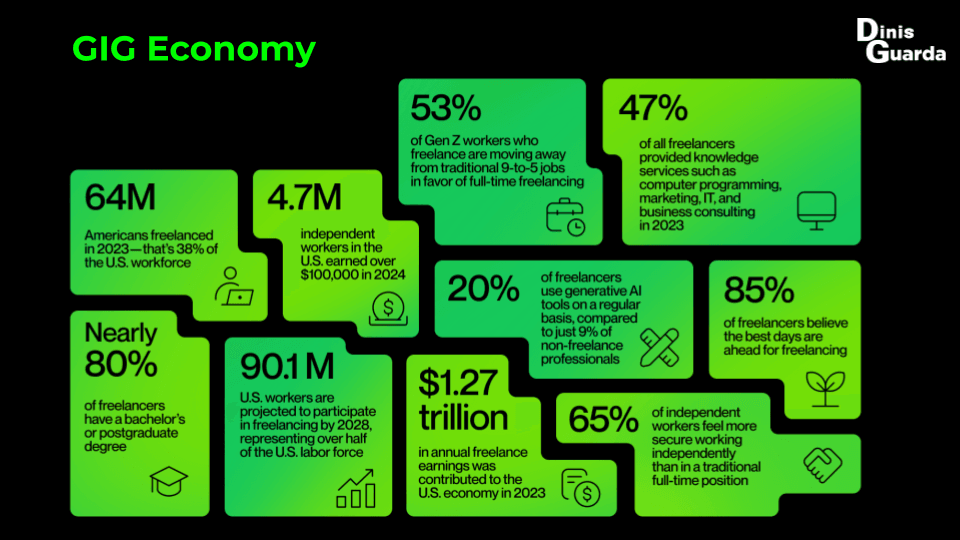

The gig economy context matters here too. In 2023, 64 million Americans freelanced, 38% of the entire US workforce, contributing $1.27 trillion to the US e,nomy. 53% of Gen Z workers who freelance are actively moving away from traditional employment. 47% of freelancers provide knowledge services including programming, marketing, and consulting. 85% believe the best days for independent work are still ahead.

These numbers point to something larger than the creator economy alone. They describe a structural shift in how people relate to work, ownership, and economic identity, one in which the creator economy and the gig economy are two expressions of the same underlying movement toward individual agency and platform-independent livelihoods.

A Map Is Not a Strategy, But You Need the Map First

The Creator Economy 360 Elements Framework does not promise easy answers. What it provides is clarity, a map of a complex, fast-moving terrain that most participants are navigating without one.

Understanding that the ecosystem runs on three interdependent pillars. Knowing that "creators" is not a monolithic category but a spectrum of profiles with different needs and paths. Accepting the 90/10 rule as a structural reality rather than a temporary obstacle. Seeing the creator economy and the gig economy as converging forces rather than separate trends. These are the foundational insights that any creator, platform, or business needs before making strategic decisions.

The second article in this series moves from landscape to strategy, examining the four-stage creator journey from attention to ecosystem ownership, the monetisation realities that separate creators who survive from those who thrive, and the vision for what a truly sustainable creator economy could look like.

This article is part of a two-part series based on Dinis Guarda's AI GIG Creator Economy Book (2025)

previous

Is Consciousness an Accident or an Inevitable Outcome?

next

Does the Concept of the Soul Still Make Sense?

Share this

Dinis Guarda

Author

Dinis Guarda is an author, entrepreneur, founder CEO of ztudium, Businessabc, citiesabc.com and Wisdomia.ai. Dinis is an AI leader, researcher and creator who has been building proprietary solutions based on technologies like digital twins, 3D, spatial computing, AR/VR/MR. Dinis is also an author of multiple books, including "4IR AI Blockchain Fintech IoT Reinventing a Nation" and others. Dinis has been collaborating with the likes of UN / UNITAR, UNESCO, European Space Agency, IBM, Siemens, Mastercard, and governments like USAID, and Malaysia Government to mention a few. He has been a guest lecturer at business schools such as Copenhagen Business School. Dinis is ranked as one of the most influential people and thought leaders in Thinkers360 / Rise Global’s The Artificial Intelligence Power 100, Top 10 Thought leaders in AI, smart cities, metaverse, blockchain, fintech.

More Articles

Blenheim Palace Brings Megalosaurus to Life Through Art, Science and Engineering

Architecture of Movement: What Deserts, Nomads and World Heritage Teach Us About Belonging

The Spiritual Meaning of the AI Singularity: What Remains Human in the Age of Artificial Intelligence?

Geometry or Pixels: Where Generative Video Belongs in a 3D Pipeline

AI Love? 50+ Million People Are Dating AI Agents

About

Where Wisdom Meets AI Utopia Edutainment

Wisdomia.ai is a 3D AI edutainment platform that seamlessly blends learning with immersive play. As the first AI-powered 3D Web 3.0 marketplace created by creators for creators. Founded by renowned serial entrepreneur and author Dinis Guarda, Wisdomia empowers individuals to flourish in an ecosystem designed for collective wisdom EQ. Join us in shaping humanity's future as we harness the power of AI to visualise and create a better world—where technology serves human potential, and innovation is guided by utopian wisdom.

Contact us

Produced by